Pension Awareness Week ran from 14 to 18 September this year. It’s a national initiative designed to get people thinking about their pension provision and their life beyond work.

Since the introduction of auto-enrolment, pension engagement – and the number of people saving for their retirement – has increased. Yet, a recent FTAdviser report confirms that ‘almost half of 22 to 29-year-olds are still not saving enough for the future.’

Whether your retirement is still decades off, or close at hand, are you saving enough to make your retirement dreams a reality?

Ask yourself these five questions.

1. Where is my retirement income coming from?

First off, think about where you expect your income in retirement to come from.

- Auto-enrolment

Introduced in 2012, auto-enrolment is a government initiative intended to encourage us to save for retirement.

For 2020/21, the minimum auto-enrolment contribution is 8% of your qualifying earnings. Qualifying earnings for the 2020/21 tax year means any pre-tax income from your employment between £6,240 and £50,000.

Your employer contributes a minimum of 3% on your behalf, leaving you to pay 5%.

You receive tax relief on your pension contributions too. This is an additional sum from the government, based on the rate of Income Tax you pay.

A basic rate taxpayer for example receives an additional £20 for every £100 they contribute. If you’re a higher or additional rate taxpayer, you receive basic rate relief but can claim back additional tax relief through your annual tax return.

The Pensions Regulator confirms that between 2012 and April 2018, auto-enrolment saw ‘the proportion of eligible staff saving into a workplace pension increase from 55% to 87%.’

If you’re auto-enrolled, are you paying the minimum contribution? If so, is that enough?

Are you expecting to receive pension income from elsewhere?

- Non-pension investments

The size of the pension contributions you make will depend partly on the size of any non-pension investments you hold.

Other income in retirement could come from tax-efficient savings, such as ISAs.

Interest from a Cash ISA is tax-free and any gains you make in a Stocks and Shares ISA are free of both Income Tax and Capital Gains Tax (CGT). The ISA allowance stands at £20,000 a year for 2020/21.

You might have other savings too – fixed-term bonds timed to pay out at retirement or income from Buy to Let properties.

If your retirement income will be supplemented by non-pension funds, be sure to factor these amounts into your retirement planning or speak to us. We can help you understood your cash flow and find the optimum contribution level for you.

- The State Pension

The State Pension won’t comprise your only pension income but at £9,110.40 for the 2020/21 tax year, you should figure it into your calculations.

To get the full new State Pension you’ll need 35 qualifying years of National Insurance Contributions.

Request a forecast to find out exactly how much your State Pension will be when you retire.

2. How much will I need?

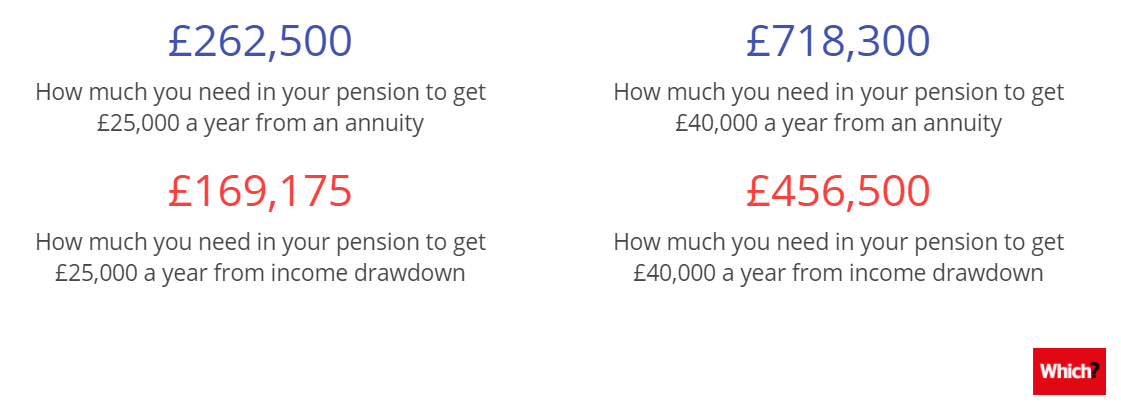

Research carried out this year by Which? confirms that retired households spend, on average, just under £2,110 a month. That’s £25,000 a year.

For retired couples living a luxurious lifestyle – one including long-haul flights and a new car every five years – the figure rises to £40,000.

The report details the size of the Defined Contribution (DC) pension pot you’d need to amass to receive these annual amounts in retirement.

Source: Which?

Notes: Annuity incomes are post-tax, joint-life amounts that also factor in receiving an annual State Pension of around £14,000 as a couple. Income drawdown amounts after tax assume savings growth of 3% annually.

The cost of retirement will be different for everyone. It’s important to think about the standard of living you expect to enjoy and plan accordingly.

Remember, the above pension funds don’t take into account any other investments you hold. You might be able to supplement your income from elsewhere. Get in touch and we can help devise a plan that allows you to meet your retirement goals.

3. When did I start saving?

As we have seen, the amount you need to contribute to your pension will depend on the income you expect to receive from elsewhere, and your aspirations in retirement.

It will also depend on the age you start saving.

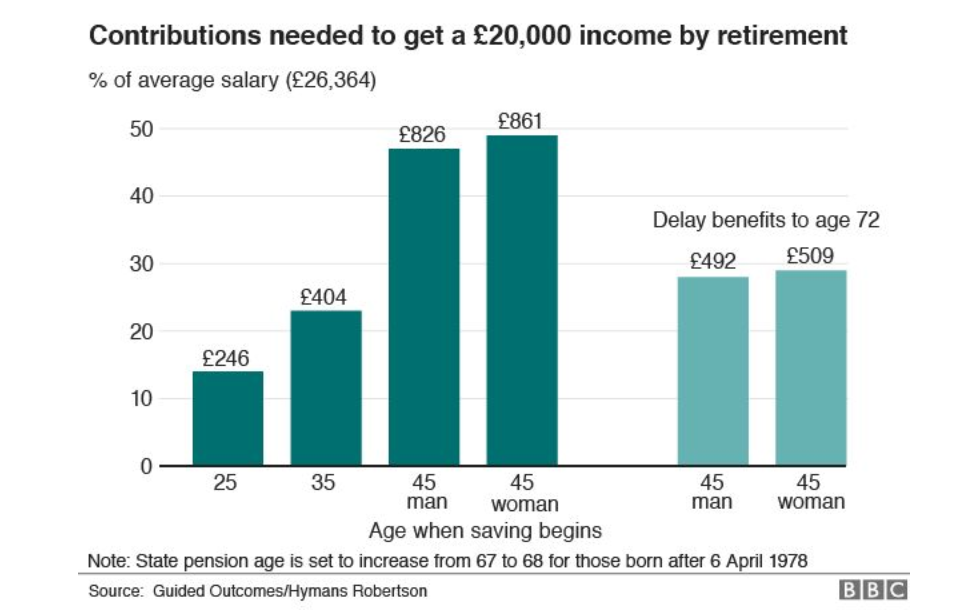

The BBC reports that to achieve a retirement income of £20,000, the average person would need to make contributions (net of tax) of £246 per month from age 25. If you are aged 45 and have only just started saving for retirement, you’ll need to contribute more – £826 per month if you are male, £861 per month if you are female.

Source: BBC

Notes: Figures assume investment growth of a typical default investment strategy and an eventual payout that increases annually with inflation, with a 50% spouse’s pension. This level of saving has a 50/50 chance of providing an annual income of £20,000 or more.

Although it’s best to start early and contribute as much as possible, a basic rule of thumb states you should contribute a percentage equal to half your age when you start contributing. If you start contributing aged 30, you should contribute 15% of your salary for the rest of your working life.

Everyone’s circumstances are different, and a rule of thumb clearly won’t be right for everyone. There are also limits to what you can contribute based on your annual income and the Annual Allowance. Speak to us if you’d like to discuss increasing your pension contributions.

4. When do I plan to retire?

The amount you need to contribute will also depend on when you plan to retire.

The State Pension age is increasing to 67 from 2028. In the same year, the minimum retirement age will rise from 55 to 57 for Defined Contribution (DC) pensions.

If you want to take benefits from age 55, your pot will need to last a lot longer.

The Office for National Statistics confirms that a male aged 65 in 2018 could expect to live for nearly 20 more years. The figure is 22 more years for a female. Retirement at 55 means your retirement fund might have to last for thirty years or more.

Depending on how you access your benefits you might also trigger the Money Purchase Annual Allowance, severely limiting the pension contributions you can make into other plans you hold, while still receiving tax relief.

5. Could I benefit from advice?

As you can see, there isn’t a ‘correct’ answer to how much you need to contribute monthly to your pension, or the size of the pot you should have when you retire.

Every individual has unique circumstances and that is where financial advice comes in. By getting to know you and your circumstances, your long-term goals, and aspirations, we can help you put together a plan that works for you.

We can help you maximise your tax-efficient savings, helping to ensure you contribute enough to your pension, whenever you plan to retire and whatever you plan to do in retirement.

Get in touch

Please get in touch if you have any questions about your retirement contributions.