Are Premium Bonds a good investment?

The government-backed National Savings and Investments (NS&I) will cut the prize pay-outs on Premium Bonds this December, reducing the prize fund from an effective interest rate of 1.4% to just 1%. This has left many asking, are Premium Bonds, still a good investment?

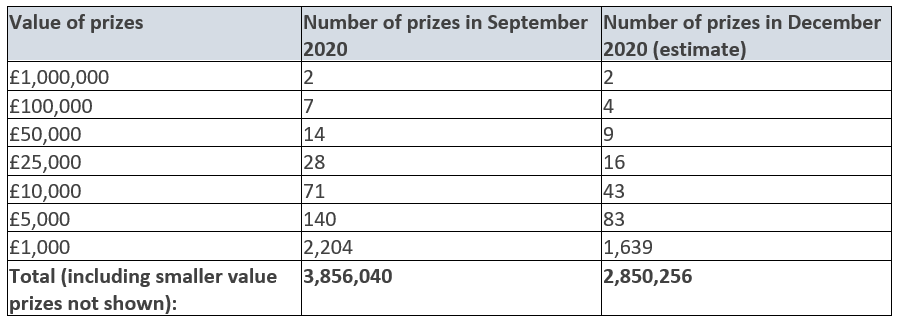

The £1 million jackpot will still be given away twice each month, but the number of £100,000 prizes will fall from seven to four. The number of chances to win all other prizes will be slashed too.

If you have savings held in a Premium Bond, either for yourself or on behalf of a loved one, what does the prize drop mean? And with even the best interest rates negligible, is it time to turn to investments rather than savings?

NS&I provide a great safety net

Introduced over 150 years ago in a bid to encourage saving, your money with NS&I is backed by HM Treasury. You are effectively lending money to the Government and for this reason, you are guaranteed not to lose your investment.

Rates of interest on NS&I products is low, especially when compared to investing in Stocks and Shares and the drop in Premium Bond prizes lowers the effective rate of interest yet further.

Premium Bonds offer a chance to win £1 million

Premium Bonds were launched in 1956. You don’t earn interest on your investment, but each £1 bond you own is entered into a prize draw with the chance to win tax-free monthly prizes.

The announcement of a drop in prizes reduces the prize fund from an effective interest rate of 1.4% to 1%. That means that the odds of a single £1 number winning a prize will decrease from 24,500-1 to 34,500-1.

Source: NS&I

Remember that if you don’t win any of the available prizes, your interest rate is essentially zero.

With the odds of winning decreased, and no interest paid, the chances of your investment not keeping pace with inflation have increased too. The money you have invested could lose value in real terms meaning that Premium Bonds may not be a good investment.

Investments could provide a good alternative to Premiums Bonds

If you are beginning to think that Premium Bonds may not be a good investment and you’re looking for an alternative to your Premiums Bonds, investments could provide the answer. The product you choose will depend on whether the Premium Bonds you held were yours, or whether you were saving for someone else – a child or grandchild for example.

You might consider:

-

An ISA

If you were holding Premium Bond savings for a child or grandchild you might consider moving those savings to a Junior ISA (JISA).

Open to anyone aged under 18, a JISA investment could be a great way to help a child save the deposit for a first home or help towards school fees.

Returns on your investment are tax-free, so no Income Tax or Capital Gains Tax will be paid on any profit that’s made and when your child or grandchild reaches the age of 18 the investment can convert into an adult ISA.

You can invest up to £9,000 into a JISA for the 2020/21 tax year.

If the savings are yours, the same tax-efficiencies apply to an adult ISA as to a JISA, but the ISA allowance is much higher.

You can invest £20,000 a year into an ISA during the 2020/21 tax year. Investing in a Stocks and Shares ISA could see much higher returns than if you leave your money in cash

-

A pension

It’s never too early to start saving for retirement.

If you’re putting money aside on behalf of a child, pensions are tax-efficient and will give them a great starting point to build on over their working life.

You can pay up to £2,880 into a pension on behalf of your child or grandchild in the 2020/21 tax year. This amount will benefit from tax relief, uplifting your investment to £3,600 per year.

The current minimum retirement age is 55 (set to rise to 57 from 2028) so the investment will be locked-in for a long time, but the returns over such a lengthy investment could make it worthwhile.

Your annual allowance is the most you can save in your pension pots in a tax year (6 April to 5 April) before you have to pay tax. You’ll only pay tax if you go above the annual allowance. This is £40,000 this tax year, or up to 100% of your pensionable earnings. Your annual allowance applies to all your private pensions, if you have more than one.

When you retire, you’ll also have the option to access up to 25% of your accumulated pension fund tax-free.

Also be aware that different allowances could apply if you have already accessed some of your pension funds flexibly, or you are a high earner. If you don’t know what allowance applies to you, get in touch.

-

A lifetime ISA

Finally, if you’re looking to help a child onto the property ladder, consider a Lifetime ISA.

Available to anyone between the age of 18 and 39, the invested amount receives a 25% bonus from the government each year. The LISA Allowance is £4,000, meaning your child could receive up to £1,000 a year from the government.

The £4,000 is taken from your child’s ISA Allowance so they can still invest £16,000 in other ISAs they hold.

The invested fund must be used to help buy your child or grandchild’s first home or left invested until after their 60th birthday. Withdrawing the money early, or for another purpose, will result in a 25% penalty.

Get in touch

Current low interest rates have resulted in a difficult time for savers. Investments offer the chance to see increased returns for you or your child, but they come with added risk too.

Please get in touch if you have any questions about your current savings or the potential for future investment.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Your pension income could also be affected by the interest rates at the time you take your benefits. Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.