As house prices continue to rise, the Office for National Statistics (ONS) recently confirmed that inflation to April 2022 had reached 9%, a 40-year high.

Now, the Office for Budget Responsibility (OBR) has blamed these two factors for an increase in its Inheritance Tax (IHT) forecast for the next five years. The government’s freeze on the nil-rate and residence nil-rate band will also be a contributing factor as estate values continue to rise.

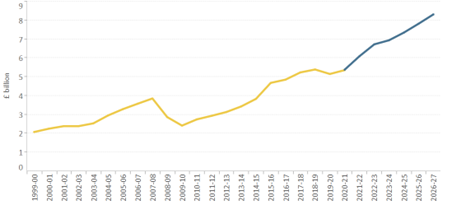

The £2.5 billion increase (compared to the OBR’s previous forecast) will see government IHT receipts hit £37 billion for the five years to 2026/27.

Source: ONS, OBR

But what does this latest forecast mean for your estate planning?

Keep reading for a look at the best ways to tax-efficiently manage your estate.

1. Understanding the “7-year rule”

IHT is paid at 40% on the value of your estate that exceeds a certain threshold.

This threshold is known as the “nil-rate band” and it is currently frozen at £325,000 until at least 2025/26. Likewise, if you pass your home onto the next generation, the residence nil-rate band could apply. Also frozen by the government, this currently stands at £175,000 and is applied to both owners if the property is jointly owned between spouses.

If you think your estate might be close to these thresholds, you can act now to lower its value, thereby decreasing the IHT liability on death.

You can make as many gifts as you want during your lifetime, but you need to survive for seven years after making the gift for it to fall outside of your estate. If you die within three years of making the gift, IHT is payable at the full 40%. Survive for between three and seven years, though, and IHT is payable on a sliding scale known as “taper relief”.

Rather than planning to distribute all of your wealth in your will, you might consider “giving while living”.

This has the benefit of increasing your chances of living for more than seven years from the date of the gift, plus you’ll still be around to see the joy your wealth brings to others.

2. You might use other HMRC gifting exemptions or give to charity

There are other ways to give tax-free gifts during your lifetime, regardless of how long you survive after giving the gift. Here are a few of the HMRC exemptions you might consider:

Annual Exemption

The Annual Exemption allows you to gift £3,000 a year tax-free, with the option to carry forward any unused amount for up to one year. The allowance applies per individual, so you and your partner could gift up to £12,000 in a single tax year if neither of you used the previous year’s allowance.

Normal expenditure out of income

If you want to make regular gifts – into a beneficiary’s JISA or pension, for example – you can make use of the normal expenditure out of income exemption.

The gifted amount must be part of your normal expenditure, made from income, and not detrimentally affect your standard of living. You should also be prepared to prove these points to HMRC if asked.

Gifts to qualifying charities

Not only can donating to charity help a cause you care about, but it can have tax advantages for you too.

Gifts to qualifying charities are free of IHT. As well as lowering the value of your estate for IHT purposes, it can also decrease the rate of IHT you pay. Donate more than 10% of your net estate to charity and HMRC will lower the IHT rate on any value that remains above the threshold from 40% down to 36%.

3. Remember to factor in your pension

Back in December 2021, we looked at how your pension could help to lower your inheritance tax bill as unused pension funds remain outside of your estate for IHT purposes. Carefully managing your pension withdrawals could have important tax implications.

If you die before age 75, any unused pension funds you hold will pass to your chosen beneficiary tax-free. Your beneficiary can choose how they take those funds, but they must claim within two years of your death to ensure tax doesn’t become payable.

On death after age 75, unused pension funds will still pass to your chosen beneficiary, but they will be taxed at the highest rate of tax they pay.

It is important to note that a pension beneficiary is appointed through your pension provider using an Expression of Wish form, rather than via your will.

If you can afford to, you might consider leaving pension funds until last – or leaving one scheme untouched – to provide a potentially tax-free inheritance to a loved one.

Get in touch

Hartsfield Planning can help you tax-efficiently manage your estate, whether through giving while living or careful retirement planning. If you would like to discuss any aspect of your estate, or your long-term financial plans, please get in touch and find out how our team of expert planners can help.

Please note

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.